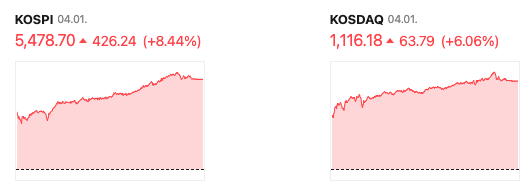

The April 2 market was shaped by a combination of rising geopolitical risk, imbalanced market flows, and sharp volatility

Rather than a simple pullback, it reflected a highly unstable environment where both external shocks and internal liquidity stress pressured sentiment

The broader index direction became less important than stock-specific and sector-specific performance

2. Escalating Geopolitical Risk

Hawkish remarks from former President Trump reignited concerns over Middle East tensions

Fears of military escalation increased as political uncertainty intensified

Reports involving military activity, including references to A-10 aircraft, deepened concerns that an actual clash could emerge over the weekend

As a result, investors leaned toward risk-off positioning rather than aggressive buying

3. Flow Imbalance and Forced Selling Risk

Market volatility became severe enough to trigger sidecars in both KOSPI and KOSDAQ for two consecutive days

A particularly concerning signal was that margin balances continued to rise even as the market declined

This suggests retail investors were maintaining or even increasing leveraged positions during the downturn

If the market falls further, this could lead to forced liquidation and margin calls, amplifying downside pressure

In other words, the main risk is not just falling prices, but the possibility of a deeper drop caused by leverage unwinding

4. Energy and Commodity Concerns

Middle East instability once again brought attention to the Strait of Hormuz risk

Potential disruption to oil and energy supply remains a burden on market sentiment

However, Korea may be somewhat protected in the short term through increased U.S. crude imports and possible pipeline rerouting by Middle Eastern producers

This means the energy risk is real, but not yet being interpreted as an immediate full-scale supply shock

5. Semiconductor View

Some parts of the market are raising concerns about a semiconductor peak-out

However, the more important factor is not the spot price but the contract price trend, which remains relatively solid

As long as earnings fundamentals stay intact, semiconductors are still seen as an area where buying on weakness may make sense

The key question is whether the recent correction reflects deteriorating fundamentals or excessive fear-driven discounting

6. Sectors in Focus

Defense / Aerospace

A sector supported by long-term structural growth

Geopolitical tension and rising global defense spending could help it outperform

Event-driven momentum such as the Artemis II mission may also support sentiment

Robotics

Tesla’s strategic shift and increasing focus on robotics may serve as a mid- to long-term catalyst

The theme could evolve beyond short-term speculation into a broader industrial transformation story

Secondary Batteries

The sector may regain attention from an energy security perspective

During market weakness, it could show relative resilience due to policy and strategic relevance

Still, a medium- to long-term approach appears more appropriate than short-term trading

7. Investment Strategy

This market favors a stock-picking environment rather than a broad index-driven rally

Excessive margin use and leverage should be avoided

Maintaining a certain level of cash and sticking to a phased buying strategy is important

Instead of chasing rebounds, investors may be better served by focusing on sectors and names backed by earnings visibility

The core strategy is clear: risk management, cash preservation, and selective accumulation

8. Final Take

On April 2, the market was pressured externally by Middle East geopolitical tensions and internally by rising leverage and distorted market flows

High volatility is likely to persist in the near term

Investors may need to focus less on the overall index and more on earnings quality, sector leadership, and balance-sheet resilience

The most practical response remains holding cash, reducing leverage, and buying in stages based on clear principles