Market expectations for Samsung Electronics have risen as major brokerages recently revised earnings consensus upward

While some investors are uncomfortable with the higher bar, analysts see it as a normal adjustment process reflecting improved outlooks

Samsung Electronics has nearly doubled over the past six months, prompting foreign investors to reduce positions as part of portfolio rebalancing

However, if the upcoming preliminary earnings meet or beat consensus, the result could become a turning point for foreign inflows to return

In that sense, the earnings release is being viewed as a key test not only for fundamentals but also for the direction of future institutional and foreign demand

2. Geopolitical risk from the Middle East

Uncertainty remains as the deadline tied to the Middle East issue has been pushed back by one day rather than fully resolved

The market is interpreting the delay as a sign that a small deal or temporary ceasefire remains possible

This keeps geopolitical risk elevated, but at the same time supports hopes for de-escalation

In addition, six Middle Eastern countries reportedly expressed their intention to prioritize crude oil supply to Korea

That signal helped ease concerns over energy supply disruption and reduced some of the pressure tied to oil-related risks

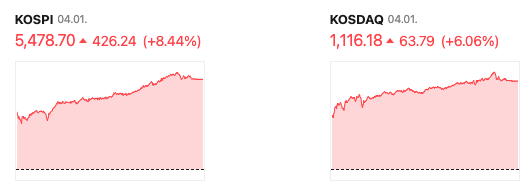

3. Weakness in KOSDAQ and notable movers

KOSDAQ underperformed KOSPI due to a mix of distorted fund flows and valuation front-loading in key sectors

Semiconductor materials, parts, and equipment names, along with secondary battery stocks, had already priced in much of the positive outlook

Volatility in major market-cap names also created ETF flow distortions, weighing on the broader KOSDAQ market

Among individual stocks, Simmtech surged on raised target prices and expectations for PCB-related demand

Danal hit the upper limit on momentum tied to AI agent-related themes

Poongsan also spiked sharply during the session on ammunition business sale-related issues

Overall, the KOSDAQ market showed a selective, theme-driven pattern rather than broad-based strength

4. Investor strategy and key takeaway

A short-term sell-the-news reaction may appear immediately after Samsung Electronics reports earnings

Still, many market participants argue that Samsung’s valuation remains attractive, with PER around 7–8x

That suggests any pullback could be seen more as a buying opportunity than a reason for panic

Investors are being advised to stay focused on principles and broader trend signals rather than reacting emotionally to daily volatility

Supportive factors such as the listing of memory-related ETFs in the U.S. also reinforce the medium- to long-term outlook for the semiconductor sector

In summary, the market may remain choppy as earnings season and geopolitical headlines intersect, but disciplined investors may still find meaningful opportunities

President Trump delivered a stark warning to Iran — threatening strong military strikes over the next 2 to 3 weeks.

But there was no ceasefire timeline. No answer to “when does this end?” And markets felt that absence immediately.

Major indices fell 1.3–1.7% at the open

WTI crude surged past $113 per barrel intraday

Investor sentiment deteriorated sharply

One speech. One morning. The whole market shaken.

2. The Hormuz Strait Toll Issue and Market Rebound

Then came an unexpected headline that shifted the mood. Reports emerged that Iran was coordinating with Oman to establish a toll collection protocol for the Strait of Hormuz.

Markets read it as a hopeful sign:

“Maybe the strait stays open after all.”

That alone was enough to spark a partial recovery.

But Wall Street analysts pushed back with cooler heads:

This is a post-war plan, not an immediate fix

GCC opposition makes it unlikely to happen anytime soon

The rebound may have been built on premature optimism

The market bought hope. But the reality remains far off.

3. Employment Data and Economic Indicators

Amid the geopolitical noise, the underlying economy held firm.

Weekly jobless claims: 202,000

Historically low — the labor market remains resilient

Eyes then turned to the next day’s March jobs report. Wall Street expected a rebound of 60,000–70,000 new positions.

Whatever is happening in the Middle East, America’s economic engine keeps running.

4. Tesla’s Sharp Decline

The day’s most dramatic mover was Tesla.

Q1 delivery numbers came in — and they missed.

Market estimate: 369,000 vehicles

Actual deliveries: 358,000 vehicles (~11,000 short)

Stock decline: -5.42%

Slowing EV demand, rising competition, and ongoing brand controversy all piled on. Investors had hoped for more. The numbers said otherwise.

5. Wall Street’s Anxiety and the Road Ahead

And yet — the market is holding. The reason? What analysts are calling the “Sako memory.”

A year ago, markets cratered on tariff fears — then roared back fast. That memory keeps investors in their seats.

“When the war ends, the market will rally hard. Don’t miss it.”

That psychology is what’s keeping Wall Street from selling out.

As Q1 earnings season approaches, the outlook splits in two:

Bulls: IT and energy earnings forecasts are being revised upward

Bears: A prolonged conflict could eventually erode corporate fundamentals

Optimism and anxiety, side by side. Wall Street is balancing on a knife’s edge.

Conclusion

Markets are holding their breath — staying invested, watching every signal. The Hormuz headlines, Tesla’s miss, the jobs data, Trump’s next words. Wall Street is absorbing it all, one volatile day at a time.

The April 2 market was shaped by a combination of rising geopolitical risk, imbalanced market flows, and sharp volatility

Rather than a simple pullback, it reflected a highly unstable environment where both external shocks and internal liquidity stress pressured sentiment

The broader index direction became less important than stock-specific and sector-specific performance

2. Escalating Geopolitical Risk

Hawkish remarks from former President Trump reignited concerns over Middle East tensions

Fears of military escalation increased as political uncertainty intensified

Reports involving military activity, including references to A-10 aircraft, deepened concerns that an actual clash could emerge over the weekend

As a result, investors leaned toward risk-off positioning rather than aggressive buying

3. Flow Imbalance and Forced Selling Risk

Market volatility became severe enough to trigger sidecars in both KOSPI and KOSDAQ for two consecutive days

A particularly concerning signal was that margin balances continued to rise even as the market declined

This suggests retail investors were maintaining or even increasing leveraged positions during the downturn

If the market falls further, this could lead to forced liquidation and margin calls, amplifying downside pressure

In other words, the main risk is not just falling prices, but the possibility of a deeper drop caused by leverage unwinding

4. Energy and Commodity Concerns

Middle East instability once again brought attention to the Strait of Hormuz risk

Potential disruption to oil and energy supply remains a burden on market sentiment

However, Korea may be somewhat protected in the short term through increased U.S. crude imports and possible pipeline rerouting by Middle Eastern producers

This means the energy risk is real, but not yet being interpreted as an immediate full-scale supply shock

5. Semiconductor View

Some parts of the market are raising concerns about a semiconductor peak-out

However, the more important factor is not the spot price but the contract price trend, which remains relatively solid

As long as earnings fundamentals stay intact, semiconductors are still seen as an area where buying on weakness may make sense

The key question is whether the recent correction reflects deteriorating fundamentals or excessive fear-driven discounting

6. Sectors in Focus

Defense / Aerospace

A sector supported by long-term structural growth

Geopolitical tension and rising global defense spending could help it outperform

Event-driven momentum such as the Artemis II mission may also support sentiment

Robotics

Tesla’s strategic shift and increasing focus on robotics may serve as a mid- to long-term catalyst

The theme could evolve beyond short-term speculation into a broader industrial transformation story

Secondary Batteries

The sector may regain attention from an energy security perspective

During market weakness, it could show relative resilience due to policy and strategic relevance

Still, a medium- to long-term approach appears more appropriate than short-term trading

7. Investment Strategy

This market favors a stock-picking environment rather than a broad index-driven rally

Excessive margin use and leverage should be avoided

Maintaining a certain level of cash and sticking to a phased buying strategy is important

Instead of chasing rebounds, investors may be better served by focusing on sectors and names backed by earnings visibility

The core strategy is clear: risk management, cash preservation, and selective accumulation

8. Final Take

On April 2, the market was pressured externally by Middle East geopolitical tensions and internally by rising leverage and distorted market flows

High volatility is likely to persist in the near term

Investors may need to focus less on the overall index and more on earnings quality, sector leadership, and balance-sheet resilience

The most practical response remains holding cash, reducing leverage, and buying in stages based on clear principles